Feature

Taiwan’s Chip Industry Outlook in the AI Race

From planning a holiday to analyzing complex datasets, generative AI is making its way into everyday life. Behind this convenience lies a pressing need for computing power, accelerating the transformation of the semiconductor industry. Taiwan, a global leader in advanced chip manufacturing, faces enormous opportunities amid this AI wave. Analysts from ITRI’s Industry, Science and Technology International Strategy Center provide an outlook on the evolving landscape.

AI semiconductors will lead industry growth over the next five years.

This growth is expected to triple the AI semiconductor market between 2024 and 2029, with GPUs remaining dominant and AI application-specific integrated circuits (ASICs) emerging as a key driver. Approximately 80% of the world’s AI chips are produced in Taiwan, making it a powerhouse for next-generation computing technologies. ITRI senior researcher Hsuan-Chih Wang estimates Taiwan’s semiconductor output will reach US$247.2 billion in 2026, an 18.3% rise from 2025. AI semiconductors powering AI servers, high-performance computing (HPC) chips—particularly from hyperscalers (large-scale cloud service providers)—will lead industry growth over the next five years.

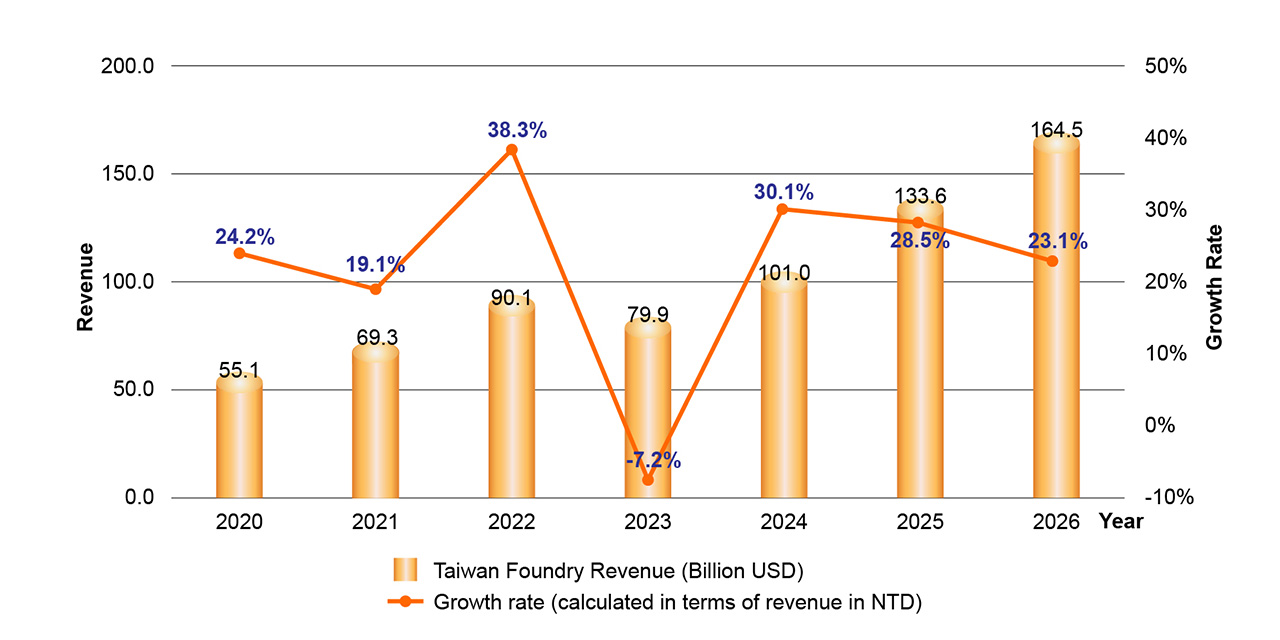

Taiwan’s Foundry Industry Revenue and Growth Rate

Following a strong 2025, ITRI projects Taiwan’s semiconductor foundry revenue to hit US$164.5 billion in 2026, a 23.1% increase primarily driven by electronic products for computing. But what will it take for Taiwan’s semiconductor industry to sustain this momentum?

Generative AI fuels unprecedented semiconductor growth.

ITRI senior researcher Nancy Liu notes that AI will evolve from digital software into physical AI embedded in devices like robots, shifting AI processing from the cloud to the edge. This transition needs a massive leap in hardware performance, specifically requiring faster algorithms, lower power consumption, near-zero latency, and high-speed memory to handle real-world physical interactions.

Competition below the 7-nanometer node is intensifying, and semiconductor development is entering the angstrom (Å) era. With denser and more thermally sensitive structures, integration of low‑temperature process flows and high‑k dielectric materials becomes essential, aligned with backside power delivery architectures. Wafer thinning will be required, but warpage mitigation is critical to sustaining yield.

Silicon photonics, which uses light instead of electricity for data transmission, is set to become a cornerstone for reducing power loss and improving bandwidth efficiency, further strengthening Taiwan’s chip innovation edge.

Advanced Packaging Powers Future Performance

With Moore’s Law slowing, advanced packaging is a critical enabler of AI performance. Jing-Han Chen, senior researcher at ITRI, highlights fan-out panel-level packaging (FOPLP) as one of the major trends. With larger surface areas and cost advantages, FOPLP is expected to overcome warpage and precision challenges by 2028, serving as a mainstream solution for advanced packaging and heterogeneous integration.

Chen also predicts that co-packaged optics (CPO) will advance to support AI and HPC, which call for high bandwidth and low power consumption. Taiwan’s strengths in silicon photonics, packaging substrates, thermal management, and testing will offer a complete value chain to support the next generation of AI applications.

Emerging Opportunities in IC Design

The AI boom has boosted ASIC design services, signaling a shift toward customized modularization and higher value-added products. Taiwan ranks second worldwide in IC design, trailing only the United States, with the two economies accounting for over 85% of the market.

“Unlike previous growth cycles led by personal computers or smartphones, this surge reflects structural demand created by generative AI,” explained ITRI researcher Sayumi Chung. “As AI models scale to trillions of parameters, data centers require unprecedented levels of computing power and memory bandwidth.”

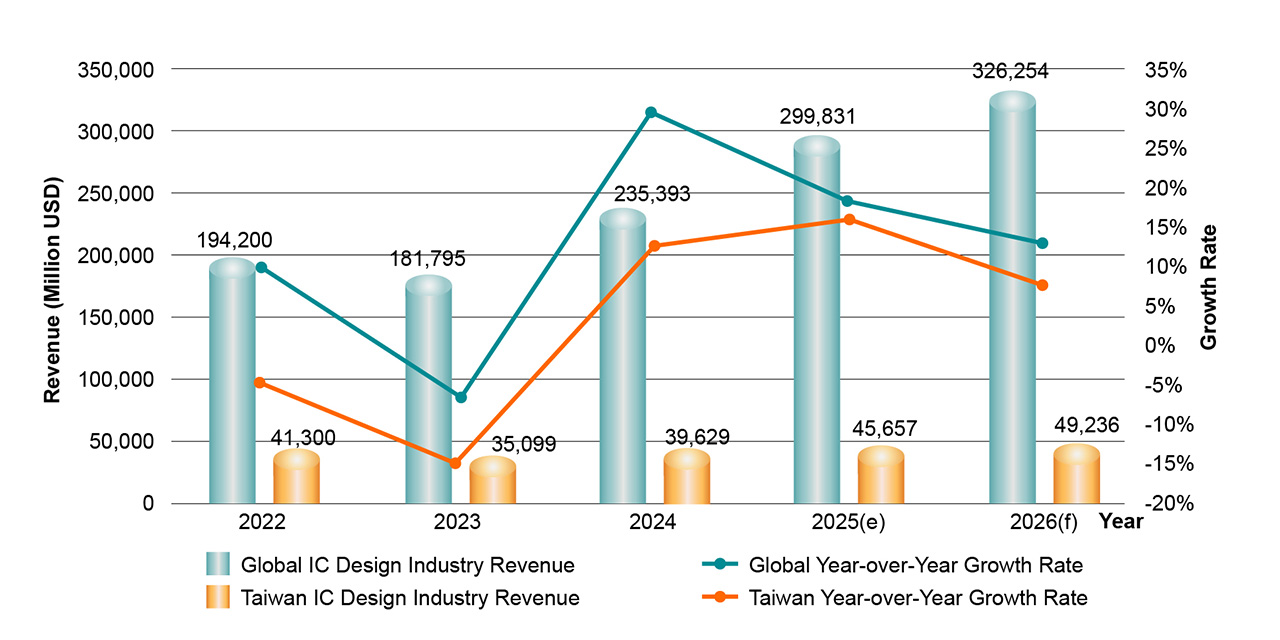

According to Chung, Taiwan’s IC design sector is projected to reach US$49.2 billion by 2026, entering a phase of slower growth but record scale. Emerging opportunities include data processing units (DPUs), edge AI, automotive chips, and AI sensors, enabling Taiwan to capture high-value segments of the AI semiconductor ecosystem.

Global and Taiwan IC design industry revenue and growth rate

The Path Forward

Generative AI is spurring computing demands and redefining the semiconductor landscape. Taiwan’s advanced process technology, world-class packaging, and dense IC design clusters position it strongly for the future. Yet the industry must also contend with technological challenges and geopolitical disruptions. How Taiwan navigates these pressures through sustained innovation, talent development, and cross-domain integration will shape its leadership in the AI race.